Over the past few months, we at Counttech have been asked by our clients to assist them in determining what government programs they eligible for and with the frequent announcements regarding new

When it comes to running a small business, hiring your first employee is one of the most exciting milestones you’ll achieve. But along with starting a new team comes the daunting task of setting up a payroll schedule.

If you’re a small business owner, you probably don’t pay much attention to the amount of paper you use every day—you’ve got a lot on your mind! But if you stop and think about it, there’s a lot of paper that goes into running a business.

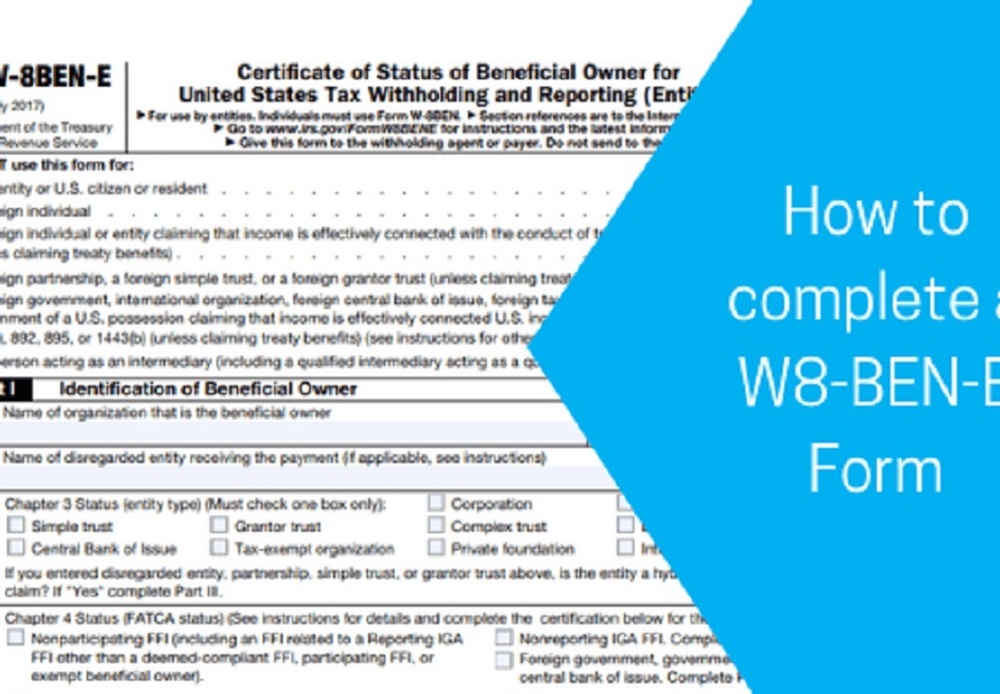

As a Canadian resident, sole proprietor or corporation working with a U.S. based customer, you might be subject to a 30% withholding tax on any payments made to you or your corporation.

As a small business owner or as an individual looking for tax advice or tax preparation services, you might have considered getting in touch with someone to take care of your accounting or tax needs.

What is cloud accounting?

Traditional accounting software is hosted locally on a computer or laptop hard drive. These software’s are typically confined to a single computer which makes it harder for a business owner to access this information.

Cloud accounting software has the same bookkeeping, payroll, and accounting functionality as a traditional accounting software’s, the difference is that the data is hosted online. Online banking is a great example of data that is available online. The cloud platform allows for data to be accessible online anytime, anywhere and from any device.

Why should small businesses consider cloud accounting?

Many small business owners get caught…

Most entrepreneurs and small business owners have no visibility into their profitability as they are deeply involved in the day to the day activities and promotion of their business. The go to solution then is to rely on part time bookkeepers and external accountants to manage books, report on profitability once a year and ensure compliance with regulatory agencies.

Although this might have worked in the past, financial statements presented at fiscal year end display historical information which does not add value or aid the business owner in making decisions that would otherwise have helped in the growth of their business…